To account for accrued revenues, an adjusting entry is made to recognize the income in the period it was earned, rather than when cash is received. This involves debiting an asset account, such as Accounts Receivable, and crediting a revenue account. By doing so, the financial statements reflect the true revenue generated during the period, providing a more accurate picture of the company’s performance. This adjustment is crucial for businesses that operate on credit terms, as it ensures that all earned income is captured in the financial records, aligning with the accrual accounting principles.

Accounting

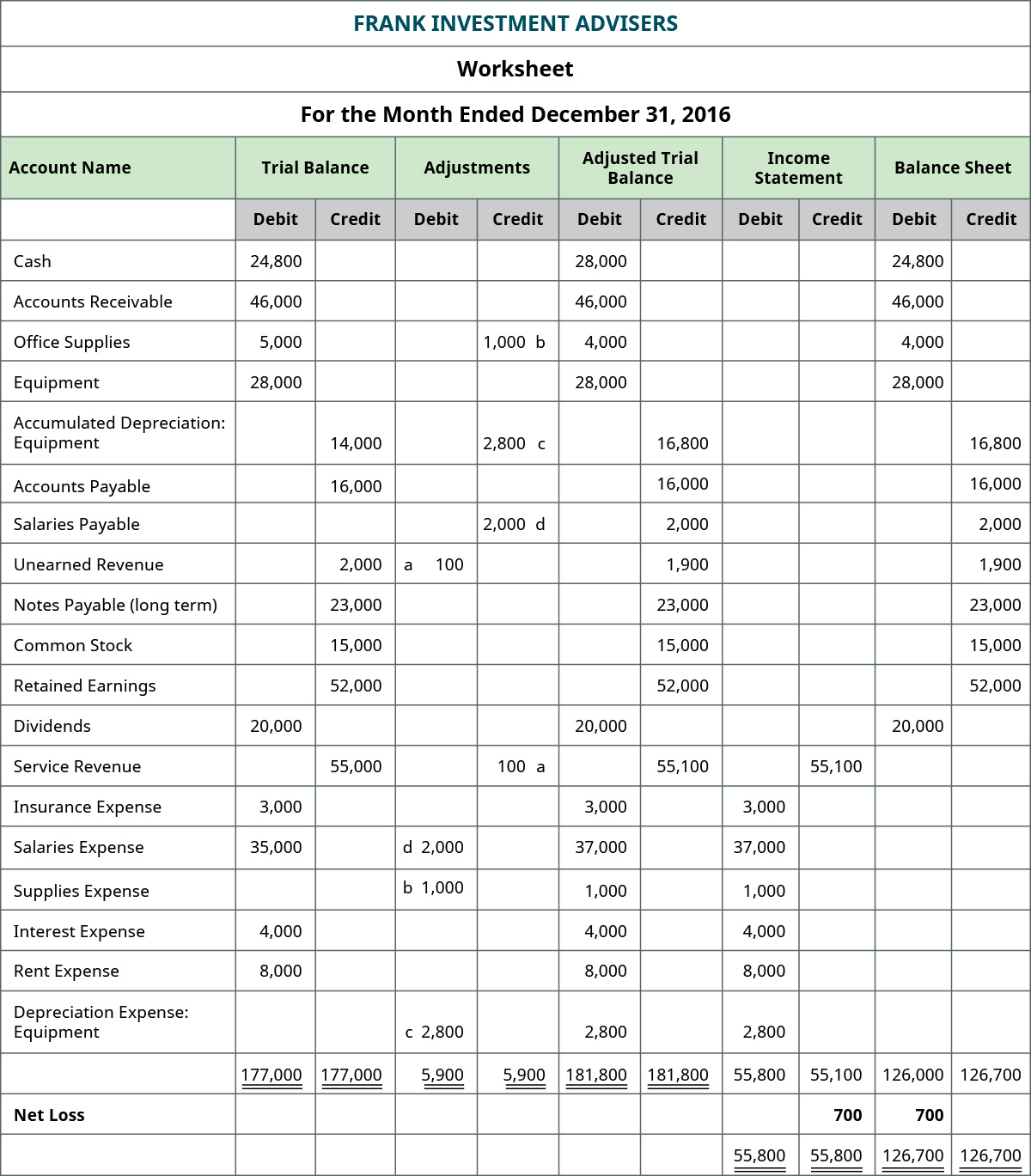

Financial statements drawn on the basis of this version of trial balance generally comply with major accounting frameworks, like GAAP and IFRS. The adjusting entries in the example are for the accrual of $25,000 in salaries that were unpaid as of the end of July, as well as for $50,000 of earned but unbilled sales. Accrued expenses – expenses incurred but not paid, i.e. represent the amount of liabilities. The next step of accounting cycle is the preparation of closing entries.

Examples of Adjusted Trial Balances

As you have learned, the adjusted trial balance is an importantstep in the accounting process. But outside of the accountingdepartment, why is the adjusted trial balance important to the restof the organization? An employee or customer may tips for taxpayers who make money from a hobby not immediatelysee the impact of the adjusted trial balance on his or herinvolvement with the company. The next type of adjustment is the accrual, which ensures inclusion of the future payments that the business entity is entitled to make.

Effective Reconciliation for Accurate Financial Management

You could also take the unadjusted trial balance and simply add the adjustments to the accounts that have been changed. In many ways this is faster for smaller companies because very few accounts will need to be altered. The second application of the adjusted trial balance has fallen into disuse, since computerized accounting systems automatically construct financial statements.

Unit 4: Completion of the Accounting Cycle

You have beentasked with determining if this transition is appropriate. After adjusting entries are made, an adjusted trial balance can be prepared. There were no Depreciation Expense and Accumulated Depreciation in the unadjusted trial balance.

Types of trial balance

Accrued expenses are costs that have been incurred but not yet paid or recorded in the financial statements. These expenses often include interest, wages, and utilities that accumulate over time. To account for accrued expenses, an adjusting entry is made to debit the appropriate expense account and credit a liability account, such as Accrued Liabilities or Accounts Payable. This adjustment ensures that expenses are recognized in the period they are incurred, in line with the matching principle. By accurately recording accrued expenses, businesses can ensure that their financial statements reflect all obligations, providing a complete picture of their financial position.

Once all the accounts are posted, you have to check to see whether it is in balance. However, most businesses can streamline this cycle and skip tedious steps like posting transactions to the general ledger and creating a trial balance. Using accounting software like QuickBooks Online can do all these tasks for you behind the scenes. Business owners and accounting teams rely on the trial balance to create reliable financial statements. A trial balance ensures the accuracy of your accounting system and is just one of the many steps in the accounting cycle.

These adjustments align the accounting records with the accrual basis of accounting, providing a comprehensive view of financial activities. Let’s delve into some of the most common adjustments encountered in this process. With the updated ledger balances in hand, you can now prepare the adjusted trial balance.

- Any difference indicates that there is accounting error in the journal entries or in the ledger or in the calculations.

- But there is some more information required to adjust the trial balance.

- This adjustment is vital for maintaining the accuracy of financial records and ensuring that all incurred costs are captured in the reporting period.

- The accounts that have been affected because of adjusting entries for the month of December are shown in red font in the adjusted trial balance.

- Three columns are used to display the account names, debits, and credits with the debit balances listed in the left column and the credit balances are listed on the right.

Trial balances come in three key types, with each serving a purpose to help create accurate financial statements. Master the essentials of preparing an accurate adjusted trial balance with practical steps and insights into common financial adjustments. The accounts that have been affected because of adjusting entries for the month of December are shown in red font in the adjusted trial balance. It is just for the purpose of explanation, and you don’t need to change the color of account titles in your homework assignments or examination questions.

Creating an adjusted trial balance is a critical step in ensuring that a company’s financial statements are accurate and reliable. By adjusting the trial balance for accrued revenues, expenses, and other necessary items, you can ensure that your financial records reflect the true state of the business. This process helps in preparing accurate financial statements and detecting any discrepancies in the accounting records. Depreciation is the systematic allocation of the cost of a tangible fixed asset over its useful life. This adjustment is necessary to account for the wear and tear, obsolescence, or reduction in value of an asset over time. To record depreciation, an adjusting entry is made to debit a depreciation expense account and credit an accumulated depreciation account, which is a contra-asset account.

Deixar Um Comentário